In the very near future of 2027, you won’t be browsing Amazon on those slow Tuesday afternoons. You won’t be comparing prices on seventeen tabs. You won’t be rage-clicking through a checkout flow that somehow still asks for your billing address even though you saved it in 2019.

Instead, an AI agent will be doing all of that for you: finding the product, verifying it's in stock, applying your loyalty points, and completing the purchase, while you are blissfully doing something else (like your actual job). The point is: you won’t be clicking "buy now." Something else will be.

That future is not even the future. Between September 2025 and May 2026, the world's largest financial institutions laid down the railroad tracks for this new era of commerce, and in Q1 2026, the trains started running.

This is the story of how the architecture of global commerce is being rebuilt at extraordinary speed, for a world where the shopper is an AI agent.

What Exactly Is Agentic Commerce?

At its simplest, agentic commerce is what happens when you hand your shopping list to an AI and say, "handle it." The agent evaluates, negotiates, and transacts. You set the parameters. The AI does the legwork. Your credit card gets charged. You get a confirmation email. The experience of shopping has been fully outsourced to software.

Unlike the familiar world of ecommerce, where you still control the final "confirm purchase" button, agentic commerce operates through delegated authority. The agent isn't advising you. It's acting for you.

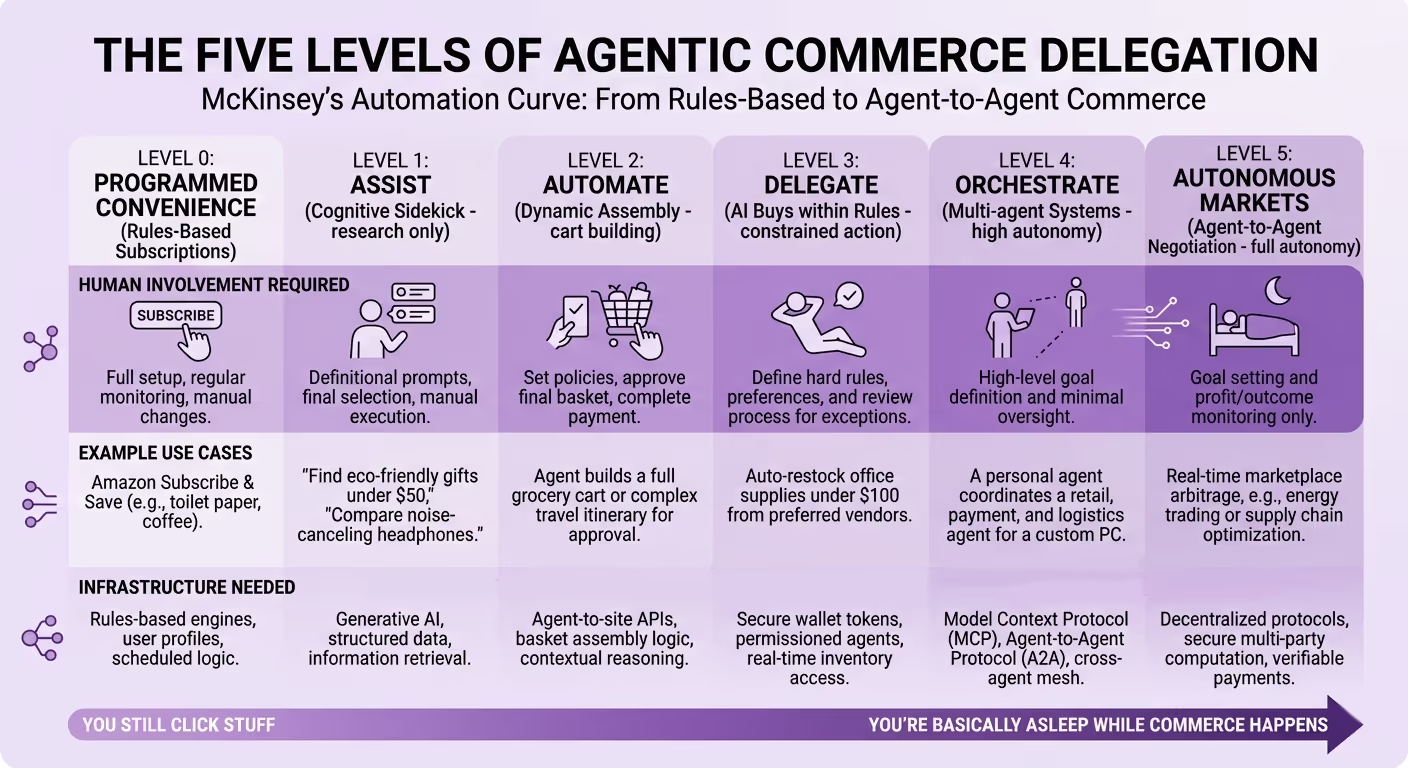

McKinsey maps this on a 0–5 "automation curve." Level 0 is your Costco subscription. Level 5 is your agent haggling with a retailer's agent in real time while you sleep. We are currently somewhere around Level 2–3, depending on the platform.

McKinsey describes this as a shift from "discrete steps" (search, browse, compare, buy) to a continuous, intent-driven flow. Your agent knows you want sneakers under $80 from a merchant with solid reviews and next-day delivery. It doesn't need a landing page. It needs a structured API, a trusted payment credential, and authorization to act.

And here's the uncomfortable implication for every ecommerce business reading this: in that world, your website is optional. The agent may never see it.

How Chatbots Accidentally Became the Gateway

AI chatbots didn't design this future. They stumbled into it and liked what they found. It started with product recommendations inside chat interfaces, which felt like a party trick. Then ChatGPT rolled out shopping features, and suddenly users were completing purchases without leaving the conversation.

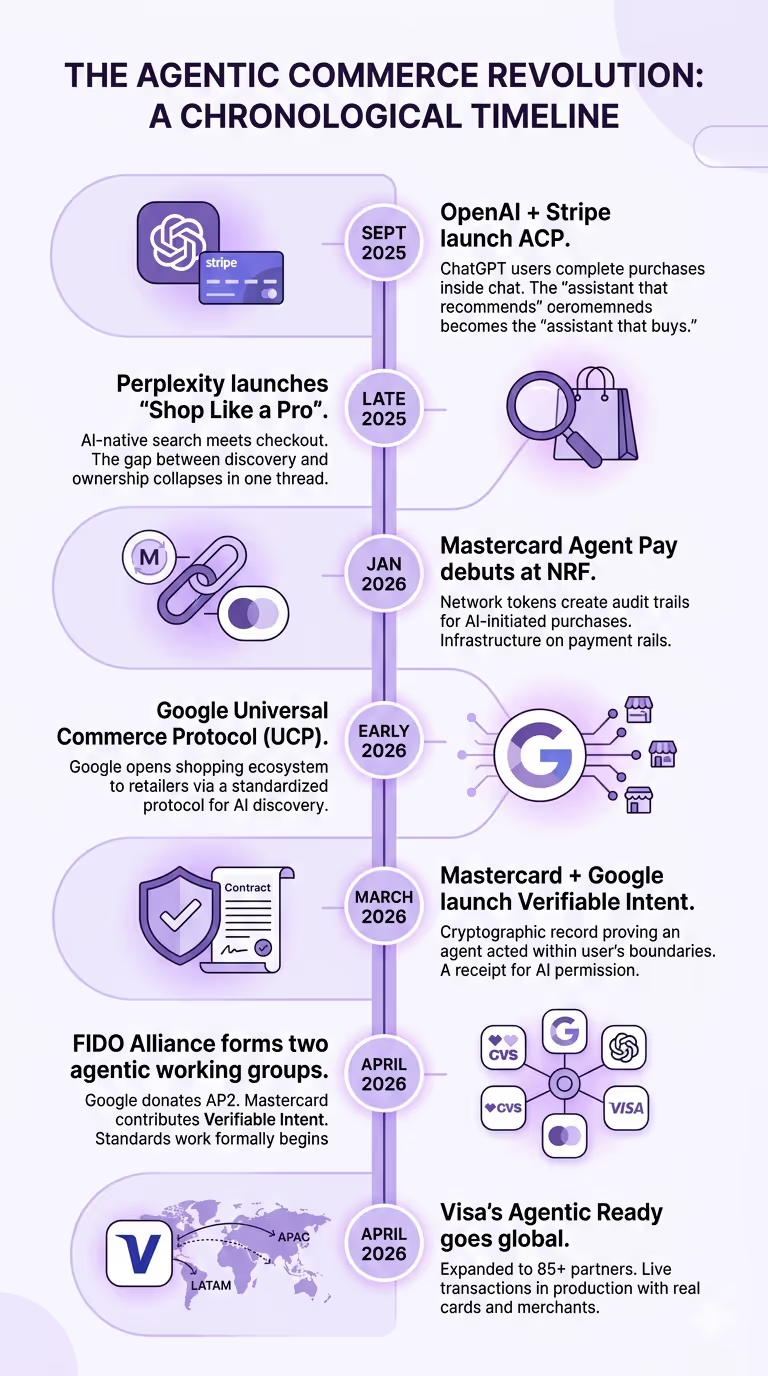

The real inflection point came in September 2025 when OpenAI and Stripe launched the Agentic Commerce Protocol (ACP). That protocol turned chatbot recommendations into chatbot transactions, a difference roughly equivalent to the gap between being told a restaurant is good and having someone make your reservation.

Here's where we actually are right now, though: most people are not handing their credit card details to an AI and walking away. They're using these tools the way they use a very well-read, very patient friend: to research, discover, evaluate, and compare. "Find me the best ergonomic chair under $400 with good reviews" is the current sweet spot. "Go buy it for me" is still a bridge most shoppers haven't crossed.

Honestly, that's not purely a trust or technology problem. People genuinely enjoy shopping. There's something deeply human about clicking "place order", the little dopamine hit, the confirmation screen, the tracking number ritual. Fully delegating that to software requires a level of faith in AI that mainstream consumers are still warming up to.

Which means the real, immediate battleground for ecommerce businesses isn't agentic checkout, it's agentic discovery. If someone asks ChatGPT, Perplexity, or Google's AI for the best option in your category and your product doesn't appear, you've lost the sale before the human ever got involved.

In a world where AI is the first stop on the shopping journey, appearing in AI search results is the new front page of Google, except most store owners haven't figured that out yet.

Why Visa, Mastercard, and Google Aren’t Sitting Back

Flashy AI interfaces are just the storefront, but the payment infrastructure is the entire building behind it. And until recently, that building didn't exist.

The core problem is trust. Specifically: how does a merchant know that an AI agent actually has permission to spend someone else's money? How does a bank verify that the "user" initiating a transaction is a legitimately authorized software agent, not a fraudster cosplaying as one? Old payment rails were built assuming a human was at the other end.

They're not great at handling "the human authorized this in advance and is currently on a hike."

Visa's Agentic Ready Program

On April 30, 2026, Visa launched its Agentic Ready program in Asia Pacific, enrolling over 50 issuing partners across 10 markets, Australia, Hong Kong, Japan, Malaysia, New Zealand, Singapore, South Korea, Taiwan, Thailand, and Vietnam. This followed an earlier European launch, and the program has already surpassed 85 partners globally.

What does "Agentic Ready" actually mean? Banks get access to a production-grade testing environment where they can validate agent-initiated payments using live cards and real merchants, before those transactions start happening at scale with their real customers. It's essentially a crash test program for AI-driven commerce.

A Visa-commissioned study found that close to 77% of Singapore residents already use generative AI tools daily, and 8 in 10 rely on AI assistance when shopping online. The infrastructure isn't theoretical, because the consumers are already there.

Mastercard's Verifiable Intent

Mastercard's contribution to this ecosystem is architectural rather than operational, and arguably more interesting for what it implies.

The Verifiable Intent framework, open-sourced and available at verifiableintent.dev, creates a cryptographic log of what a user actually authorized an AI agent to do. Not what the agent claims it was authorized to do. What the user provably, tamper-evidently, told it to do.

This solves what might be called the "the AI said it was fine" problem. Without verifiable intent, an agent could theoretically exceed its authorization and claim the user approved it. With it, every transaction carries a cryptographic receipt: here is what the user authorized, here is what the agent did, here is proof these match.

Verifiable Intent isn't built on proprietary tech, it layers on top of FIDO Alliance, EMVCo, IETF, and W3C specifications. That's deliberate: if this is going to work across the entire payments ecosystem, it can't depend on any single company's infrastructure.

Google + FIDO Alliance: Making It All Open

On April 28, 2026, Google donated its Agent Payments Protocol (AP2) to the FIDO Alliance — the same standards body that brought you passkeys, the technology that finally started killing passwords. This matters for a specific reason: handing a protocol to a standards body is categorically different from a company "opening" its API. It means no single player controls the standard. It means it evolves through community consensus. It means it's designed to be permanent infrastructure, not a competitive moat.

AP2 version 0.2, released simultaneously on GitHub, introduced support for "Human Not Present" payments: transactions where agents complete purchases without real-time human involvement, based on pre-authorized standing instructions. The example use cases are mundane but revealing: securing event tickets the instant they go on sale, replenishing household supplies when inventory hits a threshold you set, booking a restaurant when a reservation at your preferred time opens up.

Why Big Money Taking This Seriously Is the Real Story

Tech companies launch things. Standards bodies form working groups. Press releases get written. None of that alone means anything is actually happening.

But Visa and Mastercard together process the majority of global card transactions. When they dedicate engineering resources, build dedicated testing programs, and donate open standards to agentic commerce, they are making an institutional bet. These companies do not launch global programs in 10 markets because they think something might be interesting in five years. They move because the volume signals are real and the early transactions are live.

McKinsey's research projects the global agentic commerce market at $3 trillion to $5 trillion by 2030 — and critically notes that even those figures cover only goods, not services, and don't include the B2B market. The US B2C retail slice alone could reach $900 billion to $1 trillion. AI agents can use existing digital commerce infrastructure without waiting for new rails to be built.

Traffic from AI sources to retail sites has already grown 4,700% year-over-year as of mid-2025. Visitors arriving via AI agents spend 32% more time on site and are 10% more engaged than traditional visitors. The consumer behavior is shifting.

The infrastructure is catching up. The only question is whether your business is doing either of those things.

What This Actually Means for Merchants

Let's be direct: the infrastructure being built by Visa, Mastercard, Google, and the FIDO Alliance is not being built for you to look at. It's being built for AI agents to use. And if your catalog, your product data, and your checkout flow aren't compatible with agent-initiated commerce, you become invisible to a growing category of shopper.

There are three things that break in an agent-native world if you haven't prepared for them:

- Discoverability: AI agents don't browse your website. They query structured APIs. If your product data isn't machine-readable, you don't make it into the agent's consideration set. You were never there.

- Checkout compatibility: Agent-initiated payments require checkout flows that don't assume a human is present. CAPTCHA. OTPs. "Confirm you're not a robot" steps. The whole premise is that the human isn't there in the moment.

- Authorization plumbing: Protocols like ACP, UCP, and AP2 aren't optional nice-to-haves for the technically adventurous. They are the interfaces through which AI agents interact with merchants. Success at the higher automation levels requires "API-first merchandising" where inventory, pricing, shipping promises, and returns logic are cleanly exposed.

This is where Yarnit comes in. Yarnit for ecommerce is an autonomous AI engine that optimizes product catalogs specifically for agentic commerce environments. It seamlessly manages the continuous refinement required to ensure products remain discoverable, competitive, and conversion-ready within AI-native shopping interfaces.

Yarnit understands how AI agents prioritize, compare, and recommend and ensures product information aligns with the structured expectations of protocols like UCP and ACP. It also adapts catalog presentation based on how agents are actually surfacing products in live environments.

For ecommerce vendors navigating this transition, the question isn't whether to participate in agentic commerce. The question is how prepared your catalog, your data, and your checkout flows are to operate in an ecosystem where the shopper might not be human, but the purchase is still very real.

The shopper of 2028 may not click anything. The question is whether your store is ready to sell to them anyway.